Tag Archives: economics

These 7 Charts Show Why Congress Must Get Spending Under Control Immediately

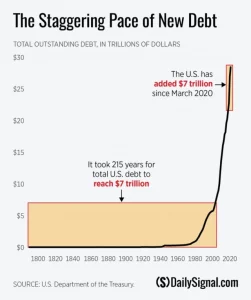

Millions of American families are reeling from the worst wave of inflation in more than four decades. [...]

12

Jul

Jul